–

MANTRAYA SPECIAL REPORT#05: 08 APRIL 2016

One Belt, One Road, One Singapore

–

Boh Ze Kai

–

Abstract

In the 14th century, Mongol dominance in Asia resulted in the Pax Mongolica, a framework of peaceful trading relationships straddling the Maritime and Overland Silk Roads, allowing the Kingdom of Singapura to flourish into a wealthy entrepot trading port. Today, the two roads are severed, and trade between Central Asia and Singapore is tiny, much more so for non-oil merchandise. The low volume of trade is evident considering Central Asia’s landlocked position presents a significant barrier of trade to the maritime trading hub that is Singapore. Today, China’s One Belt-One Road (OBOR) initiative promises to direct international attention to regional infrastructure development, effectively resurrecting a new Pax Sinica. This new economic paradigm could well create exciting new opportunities for Singaporean trade and investment in an untapped region. This report will focus on Uzbekistan, Kazakhstan and Turkmenistan, and the ways Singapore can capitalise on its unique expertise in the OBOR initiative.

–

Introduction

In 2015, Singapore exported US$61.3 million worth of goods and services to Central Asia, while importing US$6.1 million, representing 0.015 percent of Singapore’s total exports and 0.002 percent of total imports[1]; and 0.07 percent of Central Asia’s total exports and 0.009 percent of total imports[2]. While Singapore is a global trading and investment powerhouse, business experience and exposure in Central Asia has never been strong. In 2014, only 32 enterprises in Uzbekistan operated with Singaporean capital[3], and Singapore contributed only US$50 million of direct investment to Kazakhstan over the last ten years in contrast to US$604 billion of total foreign direct investment in 2014 alone[4]. Central Asia is not directly connected to Singapore, and land routes to ports in the region are scant. However, as the One Road-One Belt Initiative links Central Asia to China’s eastern seaboard, Gwadar port and even the impending sanction-free Iran; inter-regional trade is awash with new connections and opportunities.

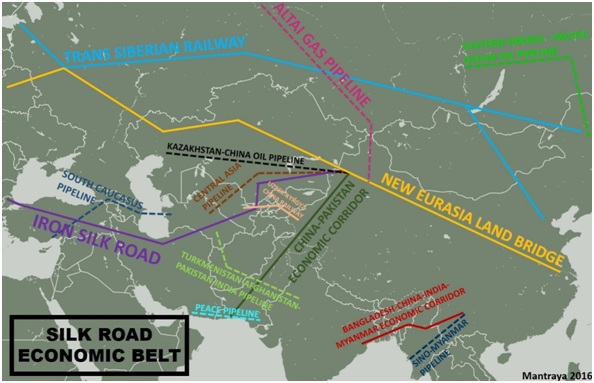

The OBOR scheme is an immense supply-side policy centring around two distinct routes that connect China to Europe. The first route, the Silk Road Economic Belt (SREB), is essentially the original Overland Silk Road through Central Asia. The cornerstone of the Belt is a motley of infrastructure projects, which will connect Urumqi to Central Asia and on to Europe. These include the Yiwu-Madrid Line completed in 2014[5] as part of the New Eurasia Land Bridge and also the Central Asia-China Pipeline, which is expected to reach operational capacity of 65Bcm/year in 2016[6](other projects detailed in Figure 2). In this way, the SREB aims to overcome the greatest challenges to trade in the region, namely skeletal transport infrastructure, crippling bureaucracy, and low levels of economic development.

The second route, the 21st Century Maritime Silk Road (MSR), is also an ancient trading system bridging China and Europe through Southeast Asia into the Suez Canal. The Road places deep emphasis on the development of ports and shipping capacity at key terminals along China’s Eastern Seaboard and the Indian Ocean. Projects including the Southeast International Shipping Centre in Xiamen, the construction of the Colombo Port City by the China Harbour Engineering Company and Gwadar Port by the China Overseas Port Holding Company aim to develop a string of international container shipping trunk hub ports radiating from South East Asia with Singapore as its lynchpin.

(Figure 1: Map of the One Road-One Belt Initiative (SREB in yellow, MSR in blue, Prepared by the author)

SINGAPORE

Location aside, Singapore also boasts some of the best trade and related services infrastructure for overseas business operations in the world. Part of the OBOR initiative envisions the use of the yuan as an international currency for business transactions, particularly in the Central Asia region, where exchange rate flux has led to high hedging costs for transactions in their own currency. As the second largest foreign offshore centre for Chinese yuan (RMB)[7] with well-cultivated business links to China, the Monetary Authority of Singapore has been quick to sell the country as a ‘Regional Gateway for RMB’[8], where Singapore-incorporated institutions have unprecedented access to RMB liquidity, enhanced trade settlement and centralised financial solutions[9]. While the initiative is chiefly targeted at the ASEAN region, there is also an opportunity for Singapore to ride on a wave of OBOR-backed investment and development to penetrate Central Asia’s gradually liberalising financial markets.

The establishment of the Singapore International Commercial Court in January 2015 cemented Singapore’s position as a regional hub for legal services, a sector which has grown 7 percent each year over the last six years[10]. The ability to conduct international arbitration and higher levels of disputes demonstrates the sophistication of Singapore’s legal devices. Chinese businesses in particular, who have long felt ostracised in traditional British or American international legal settings, are likely to trust and respect Singaporean proceedings. Due to the prevalence of State-Owned Enterprises, cross-border dispute settlement in Central Asia has relied primarily on the International Centre for the Settlement of Investment Disputes (ICSID) with energy related cases notably carried out under the auspices of the Energy Charter Treaty. Nonetheless, deeply entrenched corruption and monolithic governance has negatively impacted the rule of law throughout the region. In 2015, the Rule of Law Index ranked Kazakhstan (65), Kyrgyzstan (74) and Uzbekistan (81) among the lowest among 102 countries; primarily due to lack of government constraints and corruption[11]. Among the cases brought to the ICSID, Metal-Tech Ltd. v Republic of Uzbekistan (ICSID Case No. ARB/10/13)stands out, as the court was deemed to have had no jurisdiction due to evidence of graft. Governments must commit to anti-corruption practices over time to improve the investment climate.

The cornerstone of OBOR is transport and capacity infrastructure, and Singapore has long been a leader in the second field. In 2014, Ascendas-Singbridge was contracted to masterplan the new city of Amaravati in India’s Andhra Pradesh state; while Singaporean investment exceeding US$1.4 billion continue to power the development of the Tianjin Eco-City. Railway and pipeline construction projects characterise the Initiative, these have never been Singapore’s strong suit. However, Singapore is a leader in urban and industrial infrastructure projects such as water treatment and energy infrastructure, as well as logistics solutions and capacity maximisation. These, coupled with Singapore’s expertise in high-technology value-added manufacturing and industry, make it well-placed to enter Central Asian markets.

(Figure 2: Summary of Infrastructure Projects affiliated with the Silk Road Economic Belt, Prepared by the author)

KAZAKHSTAN

Kazakhstan is a developed upper middle-income country with a GDP per capita of US$24,100 (PPP, 2014). It benefits from fortuitous reserves of crude oil and petroleum gas, which account for 60 percent of GDP and 99.5 percent of the country’s exports to Singapore. Large reserves of ores and rare minerals have led to a burgeoning mining export industry accounting for 22 percent of GDP, while wheat-centred agriculture and a small manufacturing industry account for the remainder.

Kazakhstan’s economic direction is based on the Nurly Zhol economic plan, a US$24billion economic policy started in 2015 aimed at creating strong macroeconomic foundations and capitalising on the OBOR plan. Five key goals of the administration headed by Nursultan Äbishuly Nazarbayev are: 1) investment in Small-Medium Enterprises (SMEs), 2) banking sector revival, 3) development of commercial infrastructure, 4) development of transport infrastructure, 5) the construction of the EXPO-2017[12]. Singapore stands to profit from the first four.

SMEs today account for only 20 percent of Kazakhstan’s GDP, however the stated objectives of the Nurly Zhol plan are to boost this to 50 percent[13] by 2050.Trade accounts for 33 percent of all SME profiles, primarily importing consumer consumption products. In contrast, Singapore has much credibility in SME innovation, with SMEs contributing 50 percent of GDP in 2014[14]. A 2013 survey conducted by ADB determined that less than 50 percent demand was met for several manufacturing-based commodities including equipment and components, pharmaceuticals, furniture and consumables[15]. To fill the gap in demand, considerable technological investment and staff training is required to boost productive capacity and innovation, a domain in which Singaporean companies have strong expertise and experience. The possibilities here are endless, and Singaporean companies who are able to provide technological transfer or commercial development will be in great demand.

A World Bank survey in 2015 also indicated financial-based challenges, primarily poor cash flow based financing, and a lack of financial institutions with products and services meeting SME needs[16]. The financial crisis of 2008 caused ratings of local banks to crash, bringing with it the confidence of depositors. The net result is a serious demand for foreign financial institutions and structural reform. However, Singapore’s domestic banks lack the prestige to penetrate the market; and will likely lose out to bigger international banks. Rather, financial exports in terms of consultancies, instruments and other financial services may find more traction in the country.

Rail and road expansion projects will be the priorities of the infrastructure development strategy, China’s US$5.1 billion package of land infrastructure investment[17] may help connect key trade zones and hubs to the rest of the country. Nonetheless, land transport infrastructure remains outside of Singapore’s area of expertise. Singapore’s expertise lies in the air, and by occupying a key node on the northern Asia-Europe air corridor, Kazakhstan’s airports are well placed to provide a catalyst for economic development. However, cost-inefficient airport infrastructure and lack of capacity remains a rampant issue, with turn-around costs at Almaty airport up to 43 percent more expensive compared to European airports, and flight safety records five time worse than their global counterparts[18]. To improve efficiency and boost competition, Kazakhstan intends to privatise a broad portfolio of companies including large airports like Astana, Almaty and Atyrau Airports[19]. In addition, US$567 million is also slated for investment into expanding infrastructure and improving technical requirements[20]. With a portfolio of successful projects from Abu Dhabi International Airport to Chengdu Shuangliu International Airport, Singapore would be an obvious choice to develop some of the 25 large airports across Kazakhstan, enabling both passenger and freight air traffic.

Kazakhstan is one of the countries most heavily committed to the OBOR plan, and Singapore should seize the opportunity to gain a strong foothold in the region. In this endeavour, Singapore is aided by the great respect shown to the city-state at the highest levels of Kazakh government. Singaporean economic and social policies from the Public Service Commission to the Central Provident Fund have long been a model for Kazakhstan, and President Nursultan Nazarbayev has long held Lee Kuan Yew to be one of the greatest statesmen in the world. These reservoirs of goodwill may well help to overcome bureaucratic barriers and expedite Singapore’s entry into Central Asia.

UZBEKISTAN

Uzbekistan is a lower-middle income country with an economy centred on mining and agriculture, particularly gold and cotton. Galloping inflation in the 1990s resulted in uncontrolled depreciation, and at present, a large difference exists between official and black market exchange rates for the Uzbek som (UZS). As of April 2015, the official USD exchange rate stood at 2800som[21] while the black market rate was at 5000som[22]. The Uzbekistan Commodity Exchange operates with a semi-official exchange rate of about 3,200som, but companies continue to erode their profits when repatriated. If the internationalisation of RMB is achieved, OBOR related transactions may soon be made in RMB, providing a degree of stability and reducing hedging costs for investors. Singapore-Uzbek trade amounted to US$47.6million in 2013 (although it dipped to about US$23.9 million in 2014), and with an average annual GDP growth rate of 8 percent over the last five years, a critical location along the OBOR and a rich tradition of trade and industry, Uzbekistan is an opportunity waiting to happen.

Uzbekistan’s goal is to push its economy towards value-added products, capitalising on its human and natural resources. Uzbekistan has also begun a policy of establishing Special Industrial Zones (SIZ) offering tax exemption and a special currency exchange regime to companies willing to introduce introduce modern high-efficiency equipment and production lines to the industry[23]. Singaporean firms Welton International and Kito Investment have already been involved as shareholders in a sugar plant in the Angren SIZ in 2014[24].

The engineering and manufacturing sector receives special attention through the state auto investment enterprise Uzavtosanot, which has supported the automobile industry now accounting for 8 percent of the country’s GDP. Uzbekistan aims to localise the entire production line for automobiles, investing US$87.4 million in 2014 to the production of raw materials, chemicals and constituent parts of these vehicles[25]. Identifying the need for foreign investment and technology transfer, Uzavtosanot has already attracted US$173million of foreign investment in automobile parts production, representing the country’s second largest investment sector after geology, energy and metallurgical industries[26]. Singapore has no domestic motor vehicle industry, but due to its experience as a production hub for transnational electronics corporations, it is a major automotive component hub. Uzbekistan would do well to woo Singaporean technological and administrative expertise in order to further reduce dependency on imports for vehicle production.

Agriculture continues to account for 28 percent of Uzbekistan’s GDP, particularly its oq oltin or white gold: cotton. Uzbekistan is the world’s sixth largest producer of cotton, and exports 65 percent of its production[27]. Singapore is not suited for agricultural investment, but the difference between production and exports signifies an underdeveloped textile industry. Uzbekistan is an obvious choice as a textile production centre, with low energy costs at US$0.04/kVt, cheaply available skilled labour at US$200/month and favourable government policies including seven years of tax exemption for investment in textiles.[28] Singapore is a well-developed textile hub, but 90 percent of its US$7billion textile and apparels industry is in wholesale and retail[29], hence there would be no conflict of interest. Rather, the OBOR initiative presents the opportunity for Singapore to become a key transhipment hub on the cotton trade to non-cotton-producing countries like South Korea and Japan, while developing the pre-existing apparel and garments industry and allowing local brands to penetrate Central Asia and Russia.

While the SREB does go through Uzbekistan, unlike Kazakhstan and Turkmenistan, it does not benefit from being a major infrastructure nexus. Nonetheless, in the long history of the Silk Road, Uzbekistan has long been the richest and most innovative region, and its current poverty is actually a historical anomaly. Its high rates of growth with rich natural and human resources means as investment conditions continue to improve, it will likely attract more and more foreign investment. Singapore would be well-placed in strategic sectors to penetrate the economy at this time, and in the long-term, when Uzbekistan develops a stable service sector and greater disposable income, Singapore will be positioned to profit greatly in this developing market.

TURKMENISTAN

With 10.4 percent GDP growth, Turkmenistan is an untapped goldmine for trade and investments. Structurally, Turkmenistan is in dire need of communications and transport infrastructure. It is the key to the natural gas policy of the OBOR, envisioned to be both a main extractor and transhipment hub. Despite owning the world’s fourth largest natural gas reserves, it is the thirteenth largest producer of natural gas, indicating that most of its reserves remain untapped. Nonetheless, direct investment or any form of foreign enterprise in Turkmenistan has historically been difficult due to corruption, bureaucracy and xenophobia. Competition from nationalised corporations means that the energy industry is likely to be the only field of interest for foreign firms. Nonetheless, East Asian countries are among the best-represented among international investors. China accounts for 50 percent of all natural gas exports and owns numerous joint projects including the US$4 billion Bagtyyarlyk oilfield[30];Japan has signed a US$18 billion package of engineering contracts to develop gas fields and related industries[31]; and Malaysia’s Petronas signed a US$8 billion oil-gas investment package in 2014[32].

Despite ambitions to be a regional natural gas hub, Singaporean firms have little background in natural gas exploration or extraction operations. Rather, firms should focus on construction and energy infrastructure development. Turkmenistan is a crucial node on the SREB, with various planned pipelines originating from the country (see Figure 2), but at present, landlocked Turkmenistan has no infrastructure to export natural gas beyond the region. Cooperation with Singapore could see Turkmen gas connected to the Maritime Silk Road, facilitating strategic export towards the Asia-Pacific Region. Singapore would also be connected to a largely untapped energy-rich market, diversifying its energy pool and increasing its viability as a transit hub for energy products. With International Energy Group Singapore’s 2015 investment to develop Malta into an energy hub[33], Singapore does have the capability to provide energy-related infrastructure development in Turkmenistan.

On the administrative front, Turkmenistan presents great barriers to entry for foreign firms, with an underdeveloped legislative system, rampant corruption and the need for resilient connections at the top level of government. Singaporean firms should aim to gain a foothold in the country by riding onto consortiums with firms from other countries. This would be similar to South Korea: in 2010, LG and Hyundai entered the natural gas market riding onto the China National Petroleum Corporation consortium[34] and by 2014, the two companies signed US$4 billion worth of contracts independently[35]. Singapore’s could also join pre-established projects such as the TAPI or South Caucasus pipelines, which target to connect Turkmen gas to ports in the region.

While Turkmenistan is a country rich in resources and opportunities, the great political and investment risk associated with the country make development difficult. However, with its staunch commitment to becoming a transit hub, Turkmenistan requires infrastructure investment and must lower its barriers, creating a window with which Singapore can enter the market.

CONCLUSION

Despite the opportunities, Singapore lacks experience in the region necessary to overcome risks associated with operating in different economies based on different sets of institutions. Even Japanese, Chinese, Russian and European firms face great difficulties in their interactions with local governments and business environments. The poor experiences of the few investors in the region make the prospects of profit for risk-averse Singaporean firms challenging. A survey of 1000 Singaporean investors by BlackRock indicated that Singaporeans were more willing to accept low but guaranteed returns, and held on to unrealistic expectations regarding overseas investment[36]. This explains why the bulk of Singaporean investment is directed towards familiar markets such as ASEAN, China or the EU (65 percent in 2013).

One measure which has proved useful is the application of credit guarantee schemes, which help reduce the non-payment risks of banks in emerging markets. The Trade Finance Programme championed by the Asian Development Bank has seen US$1.7 billion worth of backed Singapore trades in 2012[37]; this has been additionally supported under the Trade Facilitation Scheme implemented jointly by International Enterprise Singapore, ADB and Swiss Re in 2015, increasing available trade finance for Singaporean firms and banks to emerging markets. This measure is primarily aimed at closer markets such as Bangladesh, Pakistan and Vietnam, but could prove useful in Central Asia as well. Nonetheless, credit limits and stricter banking rules mean that these guarantees are still not enough to meet demand, as the Republic’s emerging market trade expands three times faster than that with developing economies. Beijing-led financial institutions like the Asian Infrastructure Investment Bank and the Export-Import Bank of China may be similarly well-placed to offer similar schemes to provide financial support and attract foreign economic activity.

BIBLIOGRAPHY

Asia Development Bank. May 2013. Kazakhstan: Improving Capacity to Support SME Development. SME Survey – A Needs Assessment. Available from http://www.adb.org/sites/default/files/project-document/79676/44060-023-tacr-03.pdf. Accessed on 03 Jan 2016.

Astana Times. 09 February 2015. Kazakh Airports to get $900 million makeover. Available from http://astanatimes.com/2015/02/kazakh-airports-get-900-million-makeover/. Accessed on 15 Jan 2016.

Burgen, Stephen. 10 December 2014. The Silk Railway: freight train from China pulls up in Madrid. London: The Guardian. Available from http://www.theguardian.com/business/2014/dec/10/silk-railway-freight-train-from-china-pulls-into-madrid. Accessed on 03 Jan 2016.

Cai, Haoxiang. 27 November 2014. Singapore Investors – Cash-rich and Risk-averse. Available from http://www.businesstimes.com.sg/government-economy/singapore-investors-cash-rich-and-risk-averse. Accessed on 19 Jan 2016.

Channel News Asia. 18 August 2015. SMEs accounted for about half of Singapore’s GDP in 2014: MTI.Available from http://www.channelnewsasia.com/news/business/singapore/smes-accounted-for-about/2055118.html. Accessed on 06 Jan 2016.

Channel News Asia. 24 October 2015. Japan, Turkmenistan sign deals worth US$18b. Available from http://www.channelnewsasia.com/news/business/japan-turkmenistan-sign/2214256.html. Accessed on 06 Jan 2016.

Global Agricultural Information Network. 27 March 2014.GAIN Report: Uzbekistan – Republic of, Cotton and Products Annual 2014. Available from http://www.thefarmsite.com/reports/contents/UzbekistanCotton2April2014.pdf. Accessed on 11 Jan 2016.

GlobalEdge. 2014. Trade Statistics per Country. Michigan: International Business Centre, Michigan State University. Available from http://globaledge.msu.edu/global-insights/by/country. Accessed on 31Dec 2015.

Industrial & Commercial Bank of China. April 2015. The Introduction of RMB Internationalization and ICBC RMB Clearing bank. Beijing: Industrial & Commercial Bank of China Limited. Accessed on 18 Jan 2016.

International Energy Group Singapore. 18 May 2015. Joint Venture to Develop the Republic of Malta as a Trading Hub in the Euro-Asian Oil Trade Flow. Singapore: International Energy Group. Available from http://www.iegroup.sg/Digiland_Malta_JV_Press_Release.pdf. Accessed on 10 Jan 2016.

International Enterprise Singapore. 29 November 2013. Financing boost for exports to Asia emerging markets. Available from http://www.iesingapore.gov.sg/media-centre/news/2013/11/financing-boost-for-exports-to-asia-emerging-markets. Accessed on 19 Jan 2016.

International Journal of Research in Business Management. 07 December 2013. Free Economic Zones in Uzbekistan: the Conditions and Expected Efficiency. Tashkent: IMPACT Journals. Available from file:///C:/Users/Kai/Downloads/–1386409088-2.%20Manage-Free%20Economic-Burieva%20Nigora%20Hasanovna.pdf. Accessed on 15 Jan 2016.

Iskandar, Sanjar. 3 April 2015. Flowing conversion from poverty to destitution. Tashkent: UzMetronom. Available from http://www.uzmetronom.com/2015/04/03/plavnyjj_perekhod_ot_bednosti_k_nishhete.html. Accessed on 11 Jan 2016. Source is in Russian.

Kazakhstan 2050. 15 April 2014. Singapore invested in Kazakhstan about $50mln in 10 years. Astana: Kazakhstan2050. Available from https://strategy2050.kz/en/news/20324. Accessed on 03 Jan 2016.

Ministry for National Economy of the Republic of Kazakhstan. 05 January 2016. Complete plan for privatisation in the years 2016-2020. Available from http://economy.gov.kz/upload/Files/Celevie_indikat_real_komp_plana_privatiz_na_2016-2020g_ru.doc. Accessed on 15 Jan 2016. Source is in Russian.

Ministry of Foreign Economic Relations, Investments and Trade of the Republic of Uzbekistan. 15 January 2016. Prospective investment projects. Available from http://www.mfer.uz/ru/investments/investment-projects. Accessed on 15 January 2016. Source is in Russian.

Monetary Authority of Singapore. November 2013. Singapore: A Regional Gateway for RMB brochure – English. Available from http://www.mas.gov.sg/~/media/MAS/Singapore%20Financial%20Centre/MAS_RMB_Brochure_Website.pdf. Accessed on 18 January 2016.

National Bank for Foreign Economic Activity of the Republic of Uzbekistan. 11 January 2016. Exchange Rates. Available from http://www.nbu.com/en. Accessed on 11 Jan 2016.

Nazarbayev, Nursultan. 11 November 2014. Nurly Zhol – The Path to the Future. Astana: Embassy of the Republic of Kazakhstan. Available from http://www.kazakhembus.com/content/nurly-zhol-path-future. Accessed on 03 Jan 2016.

Nikkei Asian Review.16 June 2014. Malaysia makes $8B oil, gas investment in Turkmenistan. Tokyo: Nikkei Asian Review. Available from http://asia.nikkei.com/Business/Asean-Business-File/Malaysia-makes-8B-oil-gas-investment-in-Turkmenistan. Accessed on 09 Jan 2016.

Platts. 3 Jun 2014. Third Link of Central Asia-China Gas Pipeline to be Fully Operational by End-2015. Available fromhttp://www.platts.com/latest-news/natural-gas/singapore/third-link-of-central-asia-china-gas-pipeline-26803256. Accessed on 03 Jan 2016.

Observatory of Economic Complexity. 2014. Observatory of Economic Complexity.Massachusetts: Massachusetts Institute of Technology Media Lab. Available from http://atlas.media.mit.edu/en/. Accessed on 31 Dec 2015.

Reuters. 20 June 2014. South Korea’s LG, Hyundai clinch $4 billion deals with gas-rich Turkmenistan. London: Reuters. Available from http://www.reuters.com/article/us-gas-turkmenistan-southkorea-idUSKBN0EV1T420140620. Accessed on 10 Jan 2016.

Rule of Law Index. 2015. Kazakhstan, Kyrgyzstan & Uzbekistan. Washington D.C.: World Justice Project. Available from http://data.worldjusticeproject.org/#/groups/KYZ. Accessed on 18 Jan 2016.

State Joint-Stock Company <O’zbekyengilsanoat>. 26 May 2015. Textile industry of Uzbekistan: potential to rise and opportunities to invest. Available from http://www.jp-ca.org/navoiforum/materials/zantai/7khaidarov.pdf. Accessed on 11 Jan 2016.

Tehran Times. 02 January 2010. CNPC consortium wins $9.7billion Turkmenistan gas contract. Tehran: Tehran Times. Available from http://www.tehrantimes.com/index_View.asp?code=211081. Accessed on 10 Jan 2016.

Teo, Josephine. 27 July 2015. Speech by Senior Minister of State Mrs Josephine Teo at Plenary Luncheon of Singapore Business Federation’s Singapore Regional Business Forum on The 21st Century Maritime Silk Road on 27 July 2015. Singapore: Ministry of Transport News Centre. Available from http://www.mot.gov.sg/News-Centre/News/2015/Speech-by-Senior-Minister-of-State-Mrs-Josephine-Teo-at-Plenary-Luncheon-of-Singapore-Business-Federation-s-Singapore-Regional-Business-Forum-on-The-21st-Century-Maritime-Silk-Road-on-27-July-2015/. Accessed on 03 Jan 2016.

Textile World Asia. 17 May 2011. Singapore: A Textile Gateway. Singapore: Textile World Asia. Available from http://www.textileworld.com/textile-world-asia/twa-features/2011/05/singapore-a-textile-gateway/. Accessed on 11 Jan 2016.

The Straits Times.

Trend News Agency. 2 September 2015. Kazakhstan, China ink deals worth over $5B. Baku: Trend News Agency. Available fromhttp://en.trend.az/casia/kazakhstan/2429083.html. Accessed on 06 Jan 2016.

Trend News Agency. 11 May 2014. CNPC invests $4 billion in development of gas field in Turkmenistan. Baku: Trend News Agency. Available fromhttp://en.trend.az/business/energy/2272612.html. Accessed on 06 Jan 2016.

Tyler, Tony. 13 September 2012. IATA Aviation Day Central Asia & Caucasus, Astana, Kazakhstan. Toronto: International Air Transport Association. Available from http://www.iata.org/pressroom/speeches/Pages/2012-09-13-01.aspx. Accessed on 06 Jan 2016.

UzDaily. 30 April 2014. New sugar plant to be commissioned in SIZ Angren. Tashkent: UzDaily. Available from http://www.uzdaily.com/articles-id-27617.htm. Accessed on 18 Jan 2016.

UzReport. 24 July 2014. Uzbekistan and Singapore discussed the expansion of relations on trade and investments. Tashkent: UzReport. Available from http://news.uzreport.uz/news_2_e_122453.html. Accessed on 03 Jan 2016.

UzReport. 10 February 2015. Uzbekistan produced 245.7 thousand cars in 2014. Tashkent: UzReport.Available fromhttp://news.uzreport.uz/news_4_e_129024.html. Accessed on 15 Jan 2016.

World Bank. 5 February 2015. International Bank for Reconstruction and Development Project Appraisal Document on a Proposed Loan in the Amount of US$40 Million to the Republic of Kazakhstan for a SME Competitiveness Project. Available from http://www.adb.org/sites/default/files/project-document/79676/44060-023-tacr-03.pdf. Accessed on 03 Jan 2016.

[1] GlobalEdge (2014)

[2] Observatory of Economic Complexity (2014)

[3]UzReport (2014)

[4]Kazakhstan 2050 (2014)

[5] Burgen Stephen (2014)

[6]Platts (2014)

[7]Teo, Josephine (2014)

[8]Monetary Authority of Singapore (2013)

[9]Industrial & Commercial Bank of China (2015)

[10] The Straits Times (2015)

[11]Rule of Law Index 2015 (2015)

[12]Nazarbayev, Nursultan (2014)

[13]Nazarbayev, Nursultan (2014)

[14]Channel News Asia (2015)

[15]Asia Development Bank (2013)

[16]World Bank (2015)

[17]Trend News Agency (2015)

[18]International Air Transport Association (2012)

[19]Ministry for National Economy of the Republic of Kazakhstan (2016)

[20]Astana Times (2015)

[21]National Bank for Foreign Economic Activity of the Republic of Uzbekistan

[22]Iskandar, Sanjar (2015)

[23]International Journal of Research in Business Management (2013)

[24] UzDaily (2014)

[25]UzReport (2015)

[26]Ministry of Foreign Economic Relations, Investments and Trade of the Republic of Uzbekistan (2016)

[27]Global Agricultural Information Network (2014)

[28] State Joint-Stock Company <O’zbekyengilsanoat> (2015)

[29]Textile World Asia (2011)

[30]Trend News Agency (2014)

[31]Channel News Asia (2015)

[32]Nikkei Asian Review (2014)

[33]International Energy Group Singapore (2015)

[34]Tehran Times (2010)

[35]Reuters (2014)

[36]Business Times (2014)

[37]International Enterprise Singapore (2013)

–

–

(Boh Ze Kai is a project intern with Mantraya. This Special Report is a part of Mantraya.org’s “Borderlands” and “Regional Economic Cooperation and Connectivity in South Asia” projects.)

To Read previous Special Reports, CLICK HERE